As tensions escalate between Israel and Iran, oil prices have spiked. But according to Julius Baer’s Chief Economist Norbert Rücker, this is a sentiment-driven reaction, not a fundamental supply shock.

In a recent episode of the Beyond Markets podcast, Rücker explains why the market remains relatively calm despite the geopolitical noise, and why any oil rally may be short-lived. His message to investors: don’t overreact to headlines; fundamentals still rule.

Sentiment vs. Supply

Despite the heightened tension, Rücker argues that the current market response is more a sentiment shock than a true supply shock. This distinction matters. While oil prices have climbed, there has been no actual disruption in trade routes or infrastructure damage—two key indicators that would typically trigger lasting price shifts.

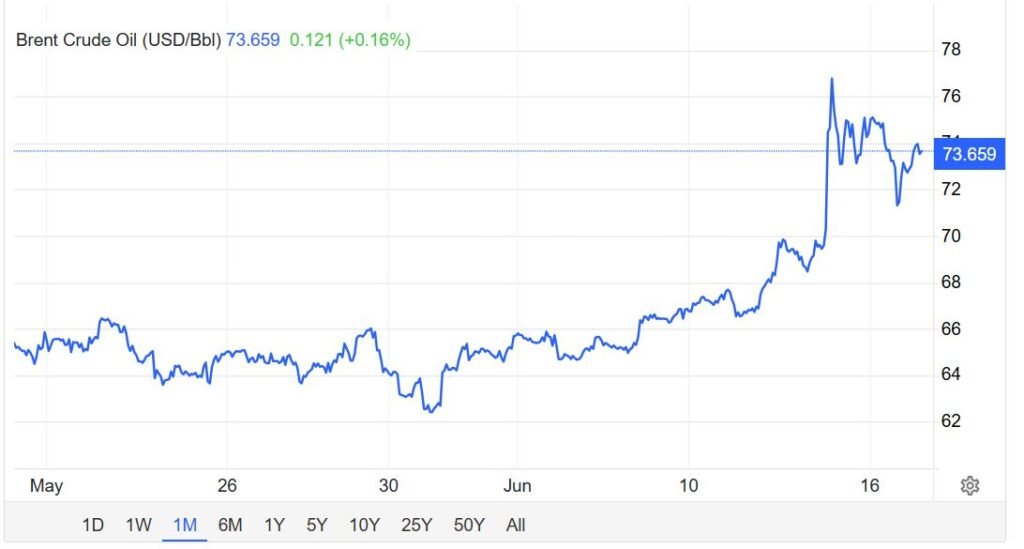

“Geopolitical risk is back,” Rücker says, “but the market’s reaction has been surprisingly unemotional.” Brent crude has hovered around the $75 mark, despite fears of a broader regional escalation.

The Strait of Hormuz—A Wildcard, But an Unlikely One

Much of the concern has centred around the Strait of Hormuz, a crucial oil chokepoint. Yet, as Rücker points out, even Iran—which relies on the route to export its own crude—has little incentive to see it closed. Shutting it down would isolate Iran from buyers like China and India, while prompting retaliatory action from the U.S. and its allies.

It’s the classic case of everyone loses, which is precisely why this scenario remains low probability.

Why This Matters for Investors

The podcast’s key insight is a cautionary one: don’t confuse headlines with fundamentals. While investors may see short-term volatility in oil and gold markets, Rücker advises not to chase price rallies based on emotion.

Instead, he recommends keeping an eye on underlying supply dynamics. There’s robust spare capacity in OPEC countries and expanding production from Brazil and Guyana. Combine that with stagnating demand (especially from China’s accelerating shift toward electrification), and you get an oil market that looks well-supplied over the next 6–12 months.

Julius Baer’s 12-month price forecast for Brent remains at USD 60 per barrel, suggesting that any rally should be viewed as temporary.

Gold: A Structurally Bullish Case

The conversation also touches on gold. While geopolitics may cause short-term spikes, the long-term tailwinds, according to Rücker, are structural. Central bank buying—especially in emerging markets—is being driven by de-dollarisation and the desire for asset diversification in a multipolar world. Gold, in his view, remains one of the few assets with both defensive and strategic appeal.

The Takeaway

This episode of Beyond Markets offers a rare blend of macro clarity and market-level nuance at a time when fear can easily overwhelm logic. For anyone looking to separate signal from noise in today’s oil and commodities market, it’s worth a listen.

🎧 Listen to the full episode here: